The PC market entered 2026 with renewed momentum: global shipments rose in 2025 on a mix of consumer demand, commercial refresh cycles, and a growing push toward AI-capable PCs—while memory and storage constraints are emerging as a key risk for 2026 pricing and volumes.

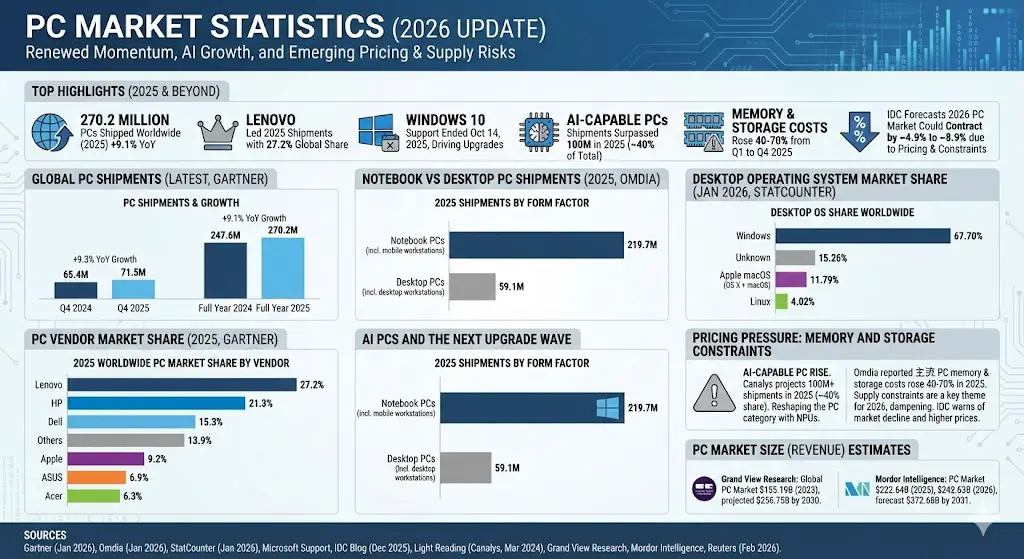

270.2 million PCs shipped worldwide in 2025 (+9.1% YoY), per Gartner’s preliminary estimates.

Q4 2025 shipments hit 71.5 million units (+9.3% YoY).

Lenovo led 2025 shipments with 27.2% global share (Gartner).

Omdia estimates 278.7 million PC shipments in 2025, including 219.7M notebooks and 59.1M desktops.

Windows held ~67.7% of worldwide desktop OS share in January 2026 (StatCounter).

Windows 10 support ended on October 14, 2025, strengthening the upgrade/refresh cycle into Windows 11.

Canalys forecast AI-capable PC shipments to surpass 100M in 2025 (~40% of all PC shipments).

IDC outlined downside scenarios where the 2026 PC market could contract by ~4.9% to ~8.9% amid memory constraints and pricing pressure.

Global PC Shipments (Latest)

Gartner’s preliminary tracker shows the PC market rebounded in 2025 after prior-year weakness, supported by upgrade-driven demand and channel inventory build ahead of component cost increases.

Period

Shipments (M units)

YoY growth

Q4 2025

71.5

+9.3%

Q4 2024

65.4

—

Full year 2025

270.2

+9.1%

Full year 2024

247.6

—

PC Vendor Market Share (2025)

In 2025, the top vendors remained stable, with Lenovo, HP, and Dell holding the top three positions by shipment share.

Bar chart: 2025 worldwide PC market share by vendor (Gartner)

Vendor

Bar

Share

Lenovo

27.2%

HP

21.3%

Dell

15.3%

Others

13.9%

Apple

9.2%

ASUS

6.9%

Acer

6.3%

Max = 27.20%. Widths: Lenovo 100.00%, HP 78.31%, Dell 56.25%, Others 51.10%, Apple 33.82%, ASUS 25.37%, Acer 23.16%.

Notebook vs Desktop PC Shipments (2025)

By form factor, notebooks remain the dominant volume driver. Omdia’s 2025 estimate puts notebooks at ~219.7M units versus ~59.1M desktops (including workstations).

Bar chart: 2025 shipments by form factor (Omdia)

Form factor

Bar

Shipments (M)

Notebook PCs (incl. mobile workstations)

219.7

Desktop PCs (incl. desktop workstations)

59.1

Max = 219.70. Widths: Notebook PCs (incl. mobile workstations) 100.00%, Desktop PCs (incl. desktop workstations) 26.90%.

Desktop Operating System Market Share (January 2026)

StatCounter’s worldwide desktop OS tracking shows Windows still leading by a wide margin. For readability, Apple’s shares are shown combined (StatCounter lists OS X and macOS separately in its breakdown).

Bar chart: Desktop OS share worldwide (Jan 2026)

Operating system

Bar

Share

Windows

67.70%

Unknown

15.26%

Apple macOS (OS X + macOS)

11.79%

Linux

4.02%

Max = 67.70%. Widths: Windows 100.00%, Unknown 22.54%, Apple macOS (OS X + macOS) 17.42%, Linux 5.94%.

AI PCs and the Next Upgrade Wave

The PC category is being reshaped by AI-capable devices (typically systems with NPUs) and by OS-driven refresh dynamics. Canalys projected AI-capable PC shipments to surpass 100 million in 2025—around 40% of all PC shipments—and to keep rising toward 2028.

At the same time, the Windows refresh cycle remains a major catalyst: Microsoft states that Windows 10 support ended on October 14, 2025, which is pushing many users and organizations toward newer hardware and Windows 11.

Pricing Pressure: Memory and Storage Constraints

Supply-side constraints are a key theme for 2026. Omdia reported that mainstream PC memory and storage costs rose by 40% to 70% from Q1 to Q4 2025, and that vendors began signaling price increases late in 2025—dampening shipment expectations for 2026.

IDC similarly warned that the memory shortage could drive higher prices and outlined downside scenarios where the PC market could decline by about 4.9% (moderate downside) to 8.9% (pessimistic downside) in 2026, alongside higher average selling prices.

Recent reporting also highlights the issue at the OEM level, with Lenovo pointing to memory shortages as a source of pressure on PC shipments and pricing.

PC Market Size (Revenue) Estimates

Revenue sizing varies by definition (some studies include tablets/hybrids alongside desktops and laptops). One estimate from Grand View Research puts the global personal computers market at $155.19B in 2023 (projecting $256.75B by 2030).

A separate estimate from Mordor Intelligence values the PC market at $222.64B in 2025 and $242.63B in 2026 (forecasting $372.68B by 2031).

Sources

Gartner (Jan 20, 2026). Worldwide PC shipments increased 9.3% in Q4 2025 and 9.1% for full-year 2025. https://www.gartner.com/en/newsroom/press-releases/2026-1-20-gartner-says-worldwide-pc-shipments-increased-9-point-3-percent-in-fourth-quarter-of-2025-and-9-point-1-percent-for-the-full-year

Omdia (Jan 12, 2026). Global PC shipments grew 9% in 2025 but memory and storage supply issues threaten 2026 outlook. https://omdia.tech.informa.com/pr/2025/dec/global-pc-shipments-grew-9percent-in-2025-but-memory-and-storage-supply-issues-threaten-2026-outlook

StatCounter Global Stats (Jan 2026). Desktop OS market share worldwide. https://gs.statcounter.com/os-market-share/desktop/worldwide

Microsoft Support. Windows 10 support ended on October 14, 2025. https://support.microsoft.com/en-us/windows/windows-10-support-has-ended-on-october-14-2025-2ca8b313-1946-43d3-b55c-2b95b107f281

IDC Blog (Dec 18, 2025). Global memory shortage crisis and potential impact on smartphone and PC markets in 2026. https://www.idc.com/resource-center/blog/global-memory-shortage-crisis-market-analysis-and-the-potential-impact-on-the-smartphone-and-pc-markets-in-2026/

Light Reading (Mar 18, 2024). AI-capable PCs forecast to make up 40% of global PC shipments in 2025 (Canalys). https://www.lightreading.com/ai-machine-learning/ai-capable-pcs-forecast-to-make-up-40-of-global-pc-shipments-in-2025-canalys

Grand View Research. Personal computers market report. https://www.grandviewresearch.com/industry-analysis/personal-computers-market-report

Mordor Intelligence. PC market report. https://www.mordorintelligence.com/industry-reports/pc-market

Reuters (Feb 12, 2026). Lenovo warns of PC shipment pressure from memory shortage. https://www.reuters.com/